Short answer: The real cost of a used heavy equipment unit includes acquisition price, reconditioning work, parts, and storage while in process. If that cost isn’t accumulated in the unit’s file from day one, the sale price is set against an incomplete cost and the calculated margin overstates actual profitability.

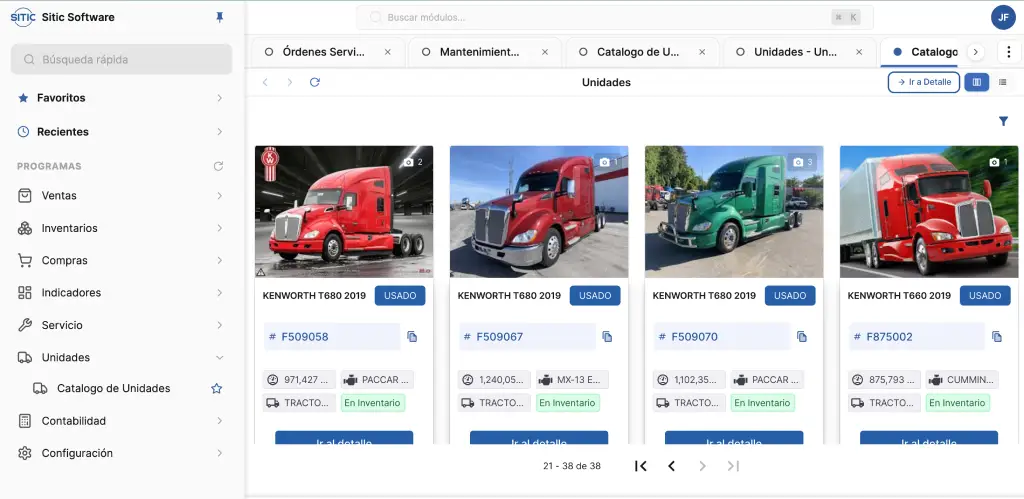

Used heavy equipment inventory is one of the most complex to manage in an entire dealership operation. Unlike new units, where the cost is defined by the manufacturer’s invoice and conditions are uniform, every used machine is a different item: it has its own operating history, its own physical condition, and its own reconditioning process before it’s ready to sell.

That heterogeneity is what makes costing errors so easy to make on used units. And costing errors on high-value equipment have significant consequences for profitability.

Why the Cost of a Used Unit Is Different Every Time

When a dealership acquires a used unit — whether as a trade-in, direct purchase, or through auction — the acquisition price is only the starting point for the real cost.

The unit typically requires a technical evaluation before knowing what condition it’s in. Depending on results, it may need anything from minor cleaning to significant reconditioning: paint, mechanical components, tires, hydraulic systems. Each of those jobs has a cost that must be allocated to that specific unit.

The real cost of the unit at the time it’s put up for sale is:

Acquisition price + reconditioning work + parts used + storage cost while in process = total unit cost

If that cost isn’t accumulated systematically in the unit’s file from the moment of acquisition, the sale price is set against an incomplete cost and the calculated margin overstates real profitability.

The Initial Valuation Is Critical

The first step in managing a used unit well is the valuation at acquisition. If the unit comes in as a trade-in on a new unit sale, the value assigned to the trade-in directly determines the new sale’s margin: if the trade-in is overpaid to close the deal, the used inventory is valued above what the market will pay.

That trade-in decision requires information: how much did it cost to recondition similar units in the past, how long did they take to sell, at what price did they sell. Without a used equipment history in the system, every trade-in is valued on the salesperson’s intuition.

The Reconditioning Process as a Cost Center

Reconditioning a used unit is, for costing purposes, similar to a shop work order: there’s technician labor, there are parts and materials. The difference is that the customer isn’t external — it’s the dealership’s own inventory.

If the system doesn’t record those reconditioning orders the same way it records external service orders — with real cost captured and linked to the specific unit — the preparation cost of used units gets lost in the shop’s general cost.

Time in Inventory and Depreciation

Used units depreciate over time. A truck that entered inventory six months ago may be worth less today — not because its condition changed, but because the market has changed or demand for that specific model has dropped.

The system must give visibility into how long each unit has been in used inventory, with accumulated cost increasing over time. That visibility enables active decisions: adjust the sale price to accelerate turnover, move the unit to another location with higher demand, or identify that the accumulated cost already exceeds the market price.

Detecting that scenario early is better than detecting it after months of additional storage.

If you want to see how SITIC manages used equipment inventory in heavy equipment dealerships, schedule a demo with our team.